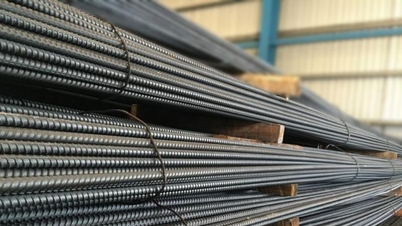

Construction steel sales in April fell by double digits to the second lowest level since 2022, despite continuous price declines.

According to the Vietnam Steel Association (VSA), construction steel sales in April reached more than 735,000 tons, down 17% from the previous month and 15% from the same period last year. This is the second lowest consumption level recorded by the market since 2022.

Poor consumption has also caused construction steel production to stagnate. In April, the country produced more than 710,000 tons, down 22% from the previous month and 37% from the same period last year. This is the lowest figure since 2022.

The April business results of Hoa Phat Group (HPG) - a company that holds about one-third of the national construction steel market share, also showed a similar situation. According to HPG's management, the demand for construction steel in Vietnam and the world remains low. This is the reason why Hoa Phat's product only reached more than 214,000 tons, down 28% compared to the same period last year. In the first 4 months, HPG sold more than one million tons of construction steel, down 34%.

The decrease in demand has caused businesses to continuously adjust steel prices. On May 19, Hoa Phat continued to reduce the price of D10 CB300 rebar by VND200,000 to VND15.09 million per ton. The reduction of VND150,000-250,000 per ton was also applied by companies such as Viet Y, Viet Duc, Southern Steel, Viet Nhat, Pomina, Tung Ho...

Thus, since the beginning of April, steel prices have dropped 6 times simultaneously. Currently, the prices of two popular steel types CB240 and D10 CB300 are around 15 million VND per ton. This price level is equivalent to the base level in October last year - the time when steel consumption demand began to decline sharply.

In a recent report, Vietcombank Securities (VCBS) also recorded that steel prices have reversed sharply since the end of April. Meanwhile, input materials have shown signs of cooling after a sharp increase, with iron ore and scrap steel returning to the low price range of 2020, and coking coal also falling amid a gradual decline in energy prices. In the coming time, the pressure to lower steel prices will remain high as demand prospects remain bleak due to high interest rates.

VCBS assessed that the residential real estate market has not recorded many real changes. The residential construction market has been negatively affected by the decline in potential supply from investors and the weakening demand for housing construction among people in the context of economic difficulties, with interest rates remaining quite high. Given the above situation, potential future supply decreased sharply in the first quarter, to a multi-year low, partly reflecting the difficulty in steel consumption demand in the following quarters.

The outlook for the domestic steel industry is likely to be in line with international forecasts. According to the World Steel Association (WSA), demand will recover by 2.3% to over 1,820 billion tonnes in 2023 and by 1.7% to over 1,850 billion tonnes in 2024. The unit noted that manufacturing is expected to lead the recovery, but high interest rates continue to weigh heavily on steel demand.

Siddhartha

Source link

![[Photo] Bustling construction at key national traffic construction sites](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/2/a99d56a8d6774aeab19bfccd372dc3e9)

![[Photo] "Lovely" moments on the 30/4 holiday](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/1/26d5d698f36b498287397db9e2f9d16c)

![[Photo] Binh Thuan organizes many special festivals on the occasion of April 30 and May 1](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/1/5180af1d979642468ef6a3a9755d8d51)

Comment (0)